RECESSIONS AND INFLATION: WHAT YOU NEED TO KNOW NOW

Spoiler Alert: This Is Not Like The Great Recession

Many people believe we are already in a recession. We are also experiencing high inflation and rising interest rates. What does that mean for our investments? What does that do to our ability to use retirement funds to provide for our lifestyle?

Can I afford to retire?

Will I have to go back to work? Finding a well-paying job sounds like an even greater obstacle as you get older.

Gas has more than doubled in the last two years. Groceries are up significantly. Home repairs and lumber have had significant increases.

Home prices and market rents have also seen significant increases over the last two years.

The cost of living is skyrocketing.

And the stock market has dropped almost 20-percent this year, so those retirement accounts can’t buy as much this year as they could a year ago.

What can we expect going forward?

Is there any hope to get back to a “normal” economy?

How can I prepare for a recession and inflation?

In order to prepare for the future, sometimes it helps to take a look at the past.

So what do you need to know now about recessions and inflation? To start, I first want to look at what a typical market cycle looks like.

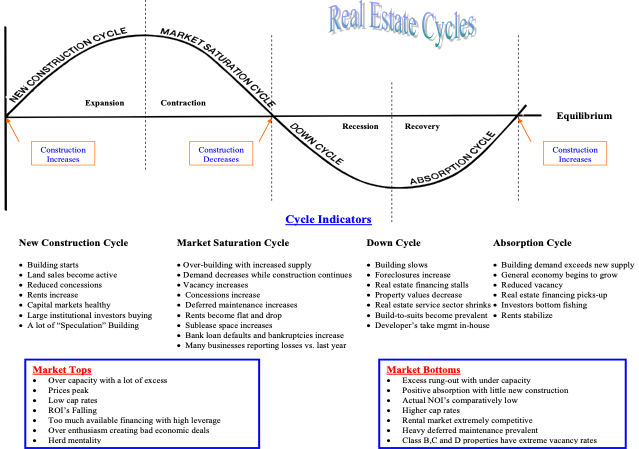

THE MARKET CYCLE

The figure below shows a typical real estate market cycle. Note that it has four phases. A complete typical cycle may last anywhere from seven to fourteen years.

Keep in mind the phases are not to scale. The Recovery Phase can be significantly longer than the Recession Phase. For example, it took about 10 years for home prices to recover from the recession that started in 2006.

Note the Cycle Indicators, which provide clues as to which phase of the market we are currently experiencing.

The Market Saturation Phase is characterized by contraction and precedes the Down Phase or Recession. Indicators include over-building with increased supply, decreasing demand while construction continues, vacancy increases and rents become flat and drop.

Some indicators of the Down Phase or Recession include a slowdown in building, foreclosures increase, real estate financing stalls, and property values decrease.

WHERE ARE WE NOW?

To determine where we are now, let’s take a look at some of the Market Tops indicators. We do not have an overcapacity of housing. A healthy market would have a 3 to 5 month supply and our supply is still less than one month.

Have prices peaked? That remains to be seen. Recent interest rate increases will put downward pressure on prices. The pool of buyers at a given price point will be smaller.

Cap rates have been low for a few years, so it is difficult to use that metric to call the top of the market. But we can expect them to go up during a recession.

Next we’ll look at the Market Saturation Phase. While the supply of housing has increased, we have not yet seen overbuilding. In fact, rents are still increasing, albeit at a slower pace. Vacancy remains low.

We know that the Federal Reserve has increased interest rates in an effort to cool the economy. Has it gone too far and triggered a recession? If so, that could accelerate the economy through the Market Saturation Phase and into the Recession Phase.

The supply of housing is still inadequate to meet the current demand. From a real estate perspective, it appears we are somewhere in the Market Saturation Phase. From a GDP, or Gross Domestic Product view, we are likely in the second quarter of a recession.

HAVE WE SEEN THIS BEFORE?

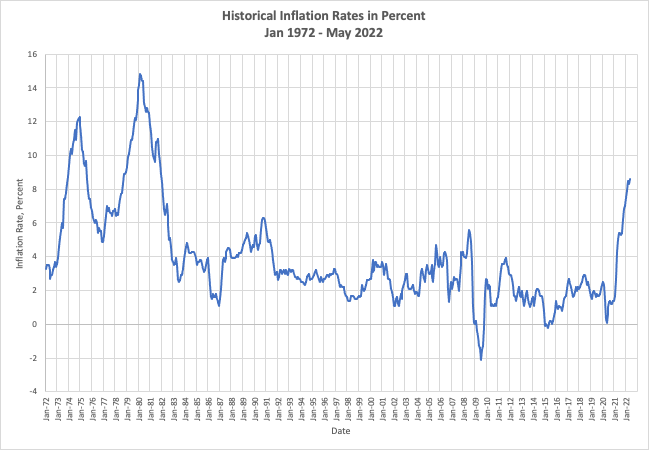

The last time we experienced inflation rising over 8 percent was in January 1979. It peaked at 14.8 percent in March 1980. To curb inflation the Federal Reserve raised interest rates. The prime rate at one point exceeded 20 percent.

The next figure shows the inflation rate for the last 50 years. This is to provide perspective. Data were obtained from https://www.usinflationcalculator.com/inflation/historical-inflation-rates/.

People still needed housing. They just had to pay more for it. So what do you think happened with home prices over the last 50 years? What do you think happened to the cost of housing during the recessions?

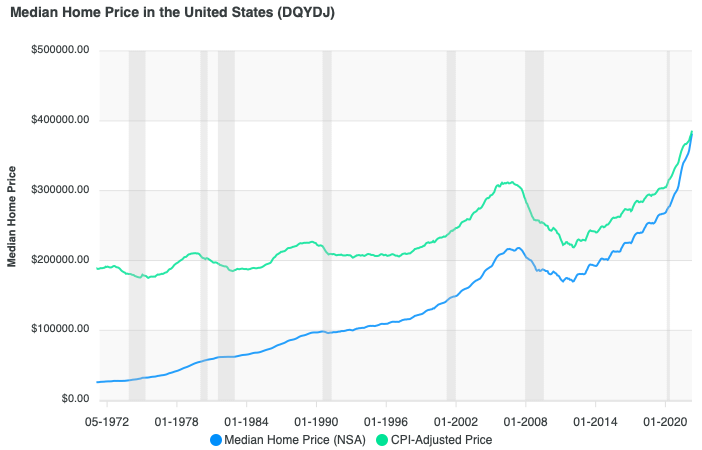

The blue line in the figure below shows the median home prices without adjusting for inflation. The gray shaded areas are recessions. Home prices remained essentially flat or increased during six of the last seven recessions. The Great Recession of 2006-2008 was the sole exception. Following the interest rate increases in 1980 and through the accompanying recession homes retained their value.

If you had a 401(k) or stock portfolio during the Great Recession, how much did it drop during the same period? Compare this to the 22-percent drop in median home price values.

Source: https://dqydj.com/historical-home-prices/

There are a number of people who did not start considering real estate as an investment until the early 2000’s. We also tend to be biased to what we have personally seen and experienced. If the only recession you remember is the Great Recession, then you could be expecting huge market value drops and a large increase in foreclosures.

Some people are afraid to buy now because they are afraid of the future. For those who consider the history of recessions, inflation and how the market recovered there will be opportunities waiting. Understanding the history of past inflationary periods and recessions helps alleviate the fear of what lies ahead.

CONCLUSION

Spiraling inflation is a threat to retirement dreams for many people. A recession can add additional fear as people wonder whether or not they will have a job or income. And they wonder if their nest egg will be enough.

What you need to know now about recessions and inflation is that they are part of a normal economic cycle. Real estate has repeatedly proven to be resilient through recessions and inflationary periods.

HELP US GET TO KNOW YOU BETTER

Attune Investments provides a better return for our investors. And we make a positive impact in people’s lives and in our world.

If you want to learn more about how others are investing with us then we invite you to join our club and request a conversation with us. See below.

We have a meetup group called Strategic Multifamily Connections. We meet once a month on the 3rd Wednesday, from 12:00 noon – 1:00 p.m. (Eastern) on Zoom. If you would like to receive the zoom links, click: MEETUP ZOOM LINKS SIGN UP

Through the power of a syndication partnership with other investors like you, working with managing partners who are experienced in managing apartment complexes, you can own multifamily assets.

Or you can choose to loan money, get in with a clear return, and get out earlier.

If you haven’t already subscribed to our BLOG, you can increase your knowledge and comfort with this asset class by subscribing now. It’s free. We publish an article every week. SUBSCRIBE HERE And take one more step. Become a member of our ATTUNE INVESTORS CLUB in which you have more personal access to us. JOIN HERE.

Mike is a retired aerospace engineer with a passion for real estate investing and teaching financial literacy. He lives with his wife in Daytona Beach, Florida.