Threat or Opportunity?

INTEREST RATES AND MULTI-FAMILY PRICING:

Threat or Opportunity?

Many people are scared or frightened. Rising inflation is eating away at their purchasing power. A $500,000 retirement nest egg doesn’t provide as much as it would have a year ago. Rising interest rates are pricing new home buyers out of the market; many of them have to keep renting or settle for much less. Investors are scared as the Federal Reserve is willing to keep raising interest rates in order to curb inflation, even if that brings on a recession.

The aggressive rate increases have created uncertainty in the housing market, both for single-family and multi-family. Some people feel like the sky is falling. Others see many foreclosures ahead.

We want to have a better understanding of what is likely ahead of us.

Let’s take a look at the effect of interest rates in the single- and multi-family sectors.

SINGLE FAMILY HOUSING MARKET

Rising interest rates have greatly reduced affordability of single-family housing. This reduced affordability has, in turn, reduced the number of qualified buyers.

Not long ago, new buyers could purchase a home with a 30-year, $300,000 mortgage with an interest rate of 3-percent. The payments would have been $1,264.81 for principal and interest. About a year later the $300,000 mortgage would have an interest rate around 6-percent, with a monthly payment of $1,798.65.

If you were a first time home buyer, what would you do? Stretch the budget for the same house? Buy less house? Or wait?

People still need housing. Many people believe they are unable to move.

Would-be sellers are unwilling to sell their current house, which may be financed at 3-percent, and buy another at 6-percent. This leads to fewer houses on the market.

A lower supply means there are not many houses for buyers to choose from. And many builders have slowed down building because of the reduced number of buyers. They don’t want their inventory sitting idle.

This is why the housing prices generally do not fall much during times of rising interest rates. There is still sufficient demand for the homes that are on the market.

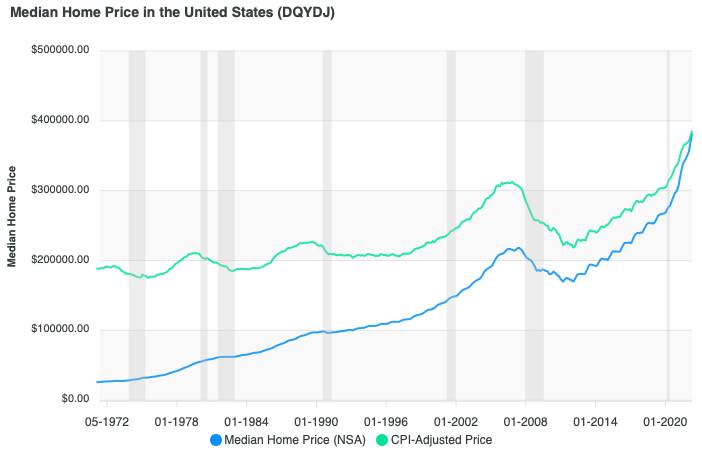

See the charts below for a comparison of median home prices and interest rates. The shaded areas are recessions. The largest interest rate increases were around 1980 and did not significantly reduce the median home price. It should be noted that home prices have dipped slightly after the last date in the first chart.

Source: https://dqydj.com/historical-home-prices/

Source: https://www.macrotrends.net/2604/30-year-fixed-mortgage-rate-chart

We also need to be aware that extrapolating effects in the single-family housing market to the multi-family market can lead to wrong conclusions. There are some significant differences.

MULTI-FAMILY HOUSING MARKET

Multi-family pricing and demand are different from single-family. The single-family home market is primarily driven by demand from people who want to live in the home. The multi-family housing market is driven by investors who require a spread between a property’s capitalization rate, or CAP rate, and the cost of financing, or interest rate.

Since we are investors, let’s take an example and see what the numbers mean.

Suppose we have a property with a Net Operating Income, or NOI, of $100,000. What would be the value if it were priced with a market CAP rate of 10-percent?

Dividing the NOI by the CAP rate we get:

$100,000 / 0.10 = $1,000,000.

It would be worth $1,000,000.

What if the market CAP rate dropped to 8-percent? We would get:

$100,000 / 0.08 = $1,250,000.

Taking it one step further, let’s suppose market demand increased and the CAP rate was driven lower to 6-percent. The value would increase to $1,666,667.

As we are aware, most multi-family buildings are not purchased with cash. There is a lender involved who is charging interest. The investor needs a spread between the cost of funds and the CAP rate. Let us suppose, for example, the spread is 2-percent.

If the interest rate on the loan is 4-percent, then the investor would require a property to be operating with a CAP rate of at least 6 percent.

If an investor purchases the property in the example above with a CAP rate of 6 percent, the initial purchase might be $1,666,667.

What happens to the price an investor will pay if interest rates go up 2 percent? Now the lender wants to charge 6-percent interest. How much would the investor pay for the same property with the same operating income? Using the numbers from above, with a 2-point spread between the interest rate and the CAP rate, investor would likely price the investment as an 8-CAP and estimate the value at $1,250,000. This is a decrease in value of $416,667 just due to the rising interest rates. That also works out to about 25-percent.

Interest rates also depend on the source and type of financing. Many single-family homes are purchased using 30-year mortgages. Loans on multi-family properties are frequently 5-7 years, with some in the 10-12 year range.

There are a number of different benchmarks that lenders use to set the interest rate. The Federal Reserve sets the Prime rate. There is also a 10-year Treasury rate. And LIBOR, or London Inter-Bank Offer Rate. These are just a few of the commonly used rates.

Many would-be buyers are currently sitting on the sidelines. And a few are buying. The rising interest rates are creating more uncertainty in the market.

If you can buy with good cash flow now, with a good spread between the CAP rate and interest rate, then the property may be a good investment. But remember that cash flow is king, and the property must generate sufficient positive cash flow to withstand market changes.

Rising interest rates in the short term will continue to put downward pressure on pricing.

Many properties have balloons coming due in the next year or two. These will need to be refinanced or purchased using funds at a higher interest rate than 5-6 years ago. The requirement to sell or refinance may be putting stress on the current owners. Some lenders may not be willing to finance in the current market.

The longer-term outlook, 2-3 years and more, should be more favorable, provided interest rates start to decline. Typically, the Federal Reserve does not raise rates during an election year. This is an observation of past activity. If high inflation persists, then you can expect the Federal Reserve to carry through on its intentions to use interest rates in its battle against inflation.

CONCLUSION

Interest rate changes have different impacts on the single-family and multi-family sectors of the real estate market. The single-family market is highly driven by a desire for home ownership and affordability of the houses available. The multi-family market is driven by investors seeking to make a profit and the cost of capital. When interest rates drop, asset prices increase. When interest rates rise, the value of those assets decreases. The spread between the cost of funds and the CAP rate of the property will be maintained and reflected in the asset’s value.

These are some of our thoughts. What do you think?

HELP US GET TO KNOW YOU BETTER

How are changing interest rates impacting your investment decisions in the current environment?

Attune Investments provides a better return for our investors. And we make a positive impact in people’s lives and in our world.

If you want to learn more about how others are investing with us then we invite you to join our club and request a conversation with us. See below.

Through the power of a syndication partnership with other investors like you, working with managing partners who are experienced in managing apartment complexes, you can own multifamily assets.

Or you can choose to loan money, get in with a clear return, and get out earlier.

If you haven’t already subscribed to our BLOG, you can increase your knowledge and comfort with this asset class by subscribing now. It’s free. We publish an article every week. SUBSCRIBE HERE And take one more step. Become a member of our ATTUNE INVESTORS CLUB in which you have more personal access to us. JOIN HERE.

Mike is a retired aerospace engineer with a passion for real estate investing and teaching financial literacy. He lives with his wife in Daytona Beach, Florida.